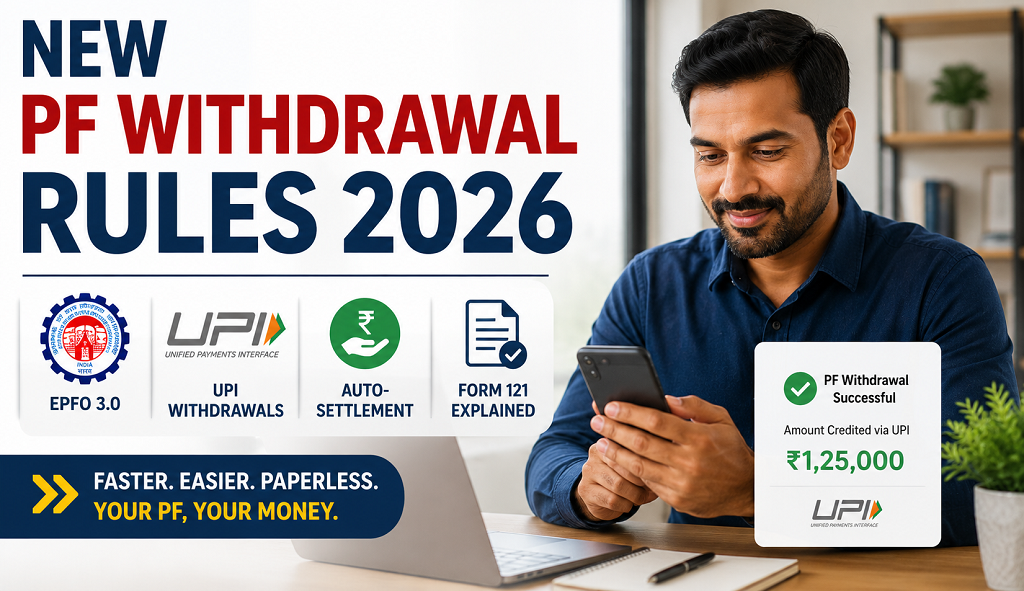

New PF Withdrawal Rules 2026 — EPFO 3.0, UPI Withdrawals, Auto-Settlement & Form 121 Explained

For most salaried Indians, the EPFO 3.0 PF withdrawal process has historically felt harder than it should. You fill a form, you wait for your employer to sign off, and then you wait again for EPFO to process it. Weeks pass before the money actually lands in your account.

That experience is changing. The new PF withdrawal rules 2026, introduced under what EPFO calls EPFO 3.0, represent the organisation’s biggest digital overhaul since the introduction of the Universal Account Number a decade ago. Higher auto-settlement limits, UPI-based access, and a sharply simplified claim structure are now replacing a system that long felt stuck in the paperwork era.

This guide explains exactly what has changed, what is already live, and what EPFO is still rolling out, so you know precisely where things stand before you file your next claim.

EPFO 3.0 PF Withdrawal Rules 2026 — Quick Overview

Here is a snapshot of the key changes before we get into the detail.

| What Changed | New Rule Under EPFO 3.0 |

| Auto-settlement limit | Raised from Rs. 1 lakh to Rs. 5 lakh |

| Employer approval | No longer required for most eligible claims |

| Withdrawal categories | Simplified from 13 categories to 3 broad types |

| Instant access | UPI and ATM-based withdrawal in final testing |

| Tax declaration form | Form 121 replaces Form 15G and Form 15H |

| Minimum balance rule | 25% of total balance must always remain |

| EPS pension waiting period | Extended from 2 months to 36 months |

What Is EPFO 3.0? The New Philosophy of Savings

EPFO 3.0 is best understood as a complete technology and process upgrade rather than a single new rule. The Central Board of Trustees approved this overhaul at its 238th meeting, with the explicit goal of making PF withdrawals function more like core banking services and less like a government paperwork process.

In practice, this means three things working together: faster automated approvals for claims that meet pre-verified conditions, fewer steps that depend on a human reviewer at EPFO’s end, and new payment channels that did not exist before, such as UPI and ATM cards. You can read the full technical details and official notifications directly on EPFO’s official website, which remains the authoritative source for any claim you file.

The rollout itself is happening in phases through 2026. Some features, such as the higher auto-settlement limit and the relaxed employer-approval rule, are already functioning. Others, including UPI and ATM withdrawals, are in advanced testing but not yet available to the public.

Old Rules vs New Rules — The 2026 Comparison

Seeing the before-and-after side by side makes the scale of this change much clearer.

| Aspect | Old System | EPFO 3.0 (2026) |

| Auto-settlement cap | Rs. 1 lakh | Rs. 5 lakh |

| Employer sign-off | Required for most claims | Not required if UAN is KYC-verified |

| Withdrawal categories | 13 separate purposes | 3 simplified categories |

| Processing time (eligible claims) | 10–20 days | Within 72 hours (auto-settled) |

| Tax form | Form 15G / 15H | Single Form 121 |

| Access method | Online claim only | Online, plus UPI/ATM (rolling out) |

Major Change #1 — Auto-Settlement Limit Raised to Rs. 5 Lakh

This is arguably the single most impactful change for ordinary salaried employees. Previously, only claims up to Rs. 1 lakh could be auto-settled by the system without manual review. Under EPFO 3.0, that ceiling has jumped to Rs. 5 lakh, which means a far larger share of withdrawal requests now bypass manual processing entirely.

Eligibility for auto-settlement depends entirely on the completeness of your KYC. Your UAN must be Aadhaar-seeded, your bank account must be verified, and your PAN should be linked as well. If you are also weighing whether to transfer or withdraw your balance after switching jobs, our detailed guide on PF transfer vs withdrawal on job change explains how this auto-settlement change interacts with the five-year continuity rule for tax-free withdrawals.

Major Change #2 — UPI and ATM-Based Withdrawals

This is the feature generating the most curiosity, and understandably so. Under the new system, EPFO intends to let members withdraw eligible funds directly through UPI apps such as PhonePe, Google Pay, and Paytm, alongside a dedicated EPFO ATM card for cash withdrawals.

As of the most recent update, testing for this feature is complete and the system is awaiting final regulatory clearances. No official launch date has been confirmed yet. Consequently, do not plan a financial decision around UPI or ATM withdrawal until EPFO formally announces that it is live. The safest way to stay updated is to keep an eye on EPFO’s official website and the UMANG app, both of which will carry the announcement the moment the feature goes public.

Major Change #3 — 13 Withdrawal Categories Simplified to 3

Anyone who has tried to withdraw PF in the past knows the frustration of figuring out which of the many specific categories — medical, marriage, education, housing, and so on — actually applies to their situation. EPFO 3.0 collapses this complexity into three broad types.

The Three Simplified Categories

- Final Settlement (Full Withdrawal) — applies on retirement, prolonged unemployment, or permanent relocation abroad

- Partial Withdrawal (Advances) — covers medical emergencies, marriage, education, housing, and similar life events under a single unified framework

- Pension Withdrawal Benefit — the EPS component, governed by its own separate rules based on years of service

Why This Simplification Matters

Fewer categories mean fewer chances of selecting the wrong claim type, which was historically one of the most common reasons claims got rejected or delayed. It also means EPFO’s backend system can apply consistent, predictable rules rather than thirteen different sets of conditions.

Major Change #4 — No Employer Approval Needed

Under the earlier system, most withdrawal claims needed your current or former employer to digitally approve the request before EPFO would process it. This single step was responsible for a large share of delays, particularly when an employee had already left the company and the employer was slow to respond.

Under EPFO 3.0, you no longer need employer approval for most eligible claims if your Aadhaar-linked UAN has verified KYC. The system accepts your verified identity as sufficient confirmation instead of relying on a third party. However, some claim types—especially first-time claims where no previous employer verified your KYC—may still require employer involvement until you fully update your records.

New Form 121 — What It Replaces

From 1 April 2026, a new self-declaration form called Form 121 came into effect under the Income Tax Act, 2025. It replaces both Form 15G, which was previously used by individuals below 60, and Form 15H, used by senior citizens, combining them into a single unified declaration.

If your total income for the financial year falls below the taxable threshold, submitting Form 121 to EPFO at the time of your claim helps you avoid TDS deduction altogether. It is worth remembering that this form must be submitted before your withdrawal is processed, since it cannot recover tax that has already been deducted. It is also only valid for one financial year, so you will need to submit a fresh form every April if your situation continues to qualify.

Understanding the 25% Minimum Balance Rule

Even with all this added flexibility, EPFO has built in a safeguard to protect long-term retirement savings. A minimum of 25% of your total PF balance, combining your contribution, your employer’s contribution, and accumulated interest, must remain in your account at all times during active service.

This floor applies across every type of partial withdrawal, including the upcoming UPI and ATM-based ones. If you want to understand exactly how your monthly contributions build up toward this balance in the first place, our PF calculation formula guide breaks down the exact percentages deducted from your basic salary each month.

EPS Pension Waiting Period — A Notable Trade-Off

Not every change under EPFO 3.0 makes things faster. One rule actually extends a waiting period rather than shortening it. Previously, members could apply for EPS withdrawal benefits after just two months of unemployment. That window has now been extended to 36 months.

The rationale behind this shift is to discourage members from cashing out their pension component prematurely during short gaps between jobs, since doing so erodes long-term retirement security. For most employees who move between jobs reasonably quickly, this change has limited practical impact. However, anyone facing a genuinely extended period without employment should factor this longer waiting period into their financial planning.

Step-by-Step — How to Withdraw PF Under EPFO 3.0

Here is the current process for filing an online PF withdrawal claim under the updated system.

- Log in to the Unified Member Portal using your UAN and password

- Navigate to Manage, then KYC, and confirm your Aadhaar, PAN, and bank account all display as Verified

- Fix any pending verification before proceeding further, since incomplete KYC is the most common reason auto-settlement fails

- Select the appropriate withdrawal category under the new simplified three-category structure

- Fill in the claim amount and purpose details accurately

- Submit Form 121 if your income falls below the taxable threshold, to avoid unnecessary TDS

- Review your claim summary carefully before final submission

- Track your claim status through the portal or the UMANG app until settlement is confirmed

Common Mistakes to Avoid Under the New Rules

- Assuming UPI or ATM withdrawal is already live — it is not, as of the latest update, so do not delay an urgent withdrawal waiting for this feature

- Leaving KYC incomplete and then being surprised when auto-settlement does not trigger

- Forgetting to submit Form 121 each financial year, resulting in avoidable TDS deduction

- Withdrawing more than the eligible 75% balance limit and having the claim rejected outright

- Not checking claim status regularly, which can delay catching an error that needs correction

Frequently Asked Questions

Do I still need employer approval for PF withdrawal?

In most cases, no, provided your UAN is fully KYC-verified with Aadhaar, PAN, and a verified bank account. A small subset of first-time claims with incomplete prior verification may still need employer involvement.

What is Form 121 and who needs it?

Form 121 is a self-declaration form introduced from 1 April 2026 that replaces the older Form 15G and Form 15H. Anyone whose annual income falls below the taxable threshold should submit it before their PF claim is processed to avoid TDS deduction.

Will this affect my PF transfer process?

No, the transfer process itself remains separate from these withdrawal changes. If you are deciding between transferring your PF to a new employer or withdrawing it after a job change, the eligibility and tax rules for transfer continue to follow the existing five-year continuity framework.

Conclusion

The new PF withdrawal rules 2026 mark a genuine shift in how EPFO interacts with its members. Faster auto-settlement, fewer paperwork dependencies, and a simplified category structure are already easing what used to be a frustrating process for crores of salaried employees. The UPI and ATM features still in testing promise to go even further once they launch.

That said, the smartest approach right now is patience paired with preparation. Get your KYC fully verified, understand which of the three simplified categories applies to your situation, and submit Form 121 if you are eligible, so that whenever you do need to make a claim, the process moves as smoothly as the new system intends. For more on related workplace rules that affect your day-to-day employment, our guide on working hours and overtime regulations in India is a useful companion read.

Reminder:

|

Post Comment