PF, ESI, gratuity laws

employee PF contribution, employer PF contribution, EPF calculation formula, EPF contribution calculation, EPF interest calculation, EPS calculation, How to calculate PF, PF calculation on salary, PF wage ceiling 15000, Provident Fund formula, Voluntary Provident Fund VPF

admin

0 Comments

PF Calculation Formula Explained – Step-by-Step Guide to EPF Calculation

If you are a salaried employee in India, you’ve probably seen a PF deduction in your salary slip every month. But have you ever actually calculated it yourself? Understanding the PF calculation formula helps you know:

-

How much you are saving

-

How much your employer contributes

-

What you’ll receive at retirement

What is Provident Fund (PF)?

Provident Fund (PF) is a government-backed retirement savings scheme where both the employee and employer contribute a fixed percentage of salary every month.

In India, this is managed by the Employees’ Provident Fund Organisation (EPFO).

Overview of EPF in India

In India, the Employees’ Provident Fund (EPF) is governed by the Employees’ Provident Fund Organisation (EPFO). It helps employees save a portion of their salary for retirement, and this savings also earn interest. The EPF covers both the employer and the employee, who each contribute a fixed percentage of the employee’s basic salary.

Role of Employees’ Provident Fund Organisation

The EPFO manages the contributions, interest, and payouts of PF accounts for salaried employees in India. They ensure the smooth operation of the system and provide necessary services like online withdrawals, transfers, and balance checks.

Why PF is Important for Salaried Employees

The PF scheme is an essential part of employee welfare, providing long-term savings for retirement, emergency needs, and unforeseen financial challenges. By contributing consistently, employees build a corpus that can help them after they retire, ensuring financial security.

PF as a Long-Term Retirement Savings Tool

PF is a secure and tax-efficient way for employees to save money. Since the system deducts contributions directly from their salary, employees often do not feel the impact of saving. Over the years, they can use the accumulated amount to provide income during retirement or in times of crisis.

What is the PF Calculation Formula?

Let’s simplify it.

The standard PF calculation formula is:

PF = (Basic Salary + Dearness Allowance) × 12%

This applies to the employee’s contribution.

Standard 12% Rule

-

Employee contributes 12%

-

Employer contributes 12%

-

Total monthly PF contribution = 24%

Applicability of Wage Ceiling (₹15,000 Rule)

If Basic + DA is:

-

₹15,000 or less → PF calculated on full salary

-

Above ₹15,000 → PF may be limited to ₹15,000 unless company allows higher contribution

This ceiling is very important in PF calculation.

Components of the PF Calculation Formula

Basic Salary

This is the fixed component of your salary before allowances.

PF is not calculated on CTC, HRA, bonuses, or special allowances.

Dearness Allowance (DA)

DA is given to offset inflation.

In many private jobs, DA may not be separate — in that case, PF is calculated only on Basic.

Contribution Rate

-

Employee Contribution = 12%

-

Employer Contribution = 12%

But the employer’s share is divided differently (explained below).

Employee and Employer PF Contribution Breakdown

Employee’s Contribution (12%)

The employee contributes 12% of their basic salary + DA toward the EPF. This entire amount is credited to the EPF account.

Employer’s Contribution (12% Split)

The employer contributes 12%, but it is split into two components:

-

8.33% is directed to the Employee Pension Scheme (EPS).

-

3.67% goes to the EPF.

-

Contribution to EDLI (Employees’ Deposit Linked Insurance) and administrative charges may also apply.

Step-by-Step PF Calculation in India

Step 1 – Calculate Employee Contribution

To calculate the employee’s PF contribution, simply multiply the total of the basic salary + DA by 12%. For example, if an employee’s basic salary + DA is ₹20,000, the employee’s contribution will be ₹20,000 × 12% = ₹2,400.

Step 2 – Calculate Employer Contribution

The employer’s total contribution is also 12%. However, only 3.67% goes to the employee’s EPF, and 8.33% is directed toward the EPS. For the same ₹20,000 salary, the employer will contribute ₹2,400 (12% of ₹20,000), with the breakdown of the contribution being ₹740 to EPF and ₹1,660 to EPS.

Step 3 – EPS Contribution Calculation

The employer contributes 8.33% of the basic salary towards the EPS, but caps the contribution at ₹1,250 per month, depending on the salary amount

Step 4 – Administrative Charges (If Applicable)

Employers may also have to pay a small fee toward the administration of the EPF, which is generally 0.5% of the total monthly wage.

PF Calculation Formula Examples (With Salary Table)

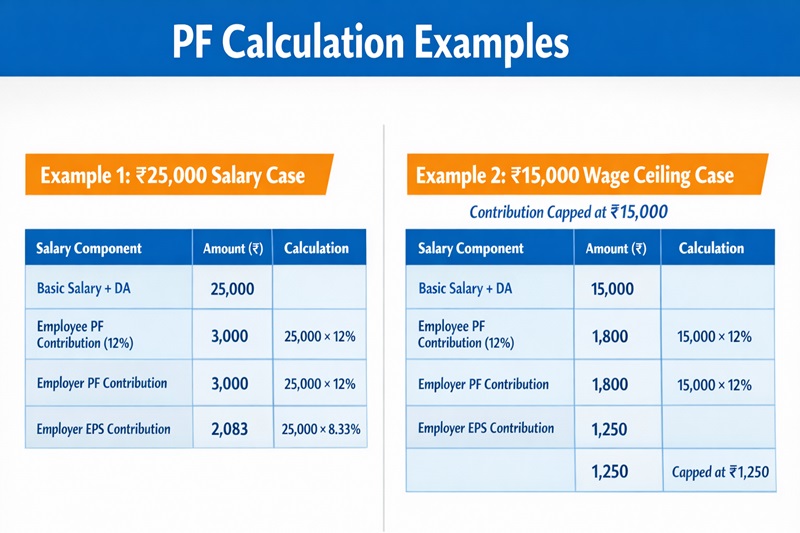

Example 1: ₹25,000 Salary Case

| Salary Component | Amount (₹) | Calculation |

|---|---|---|

| Basic Salary + DA | 25,000 | |

| Employee PF Contribution (12%) | 3,000 | 25,000 × 12% |

| Employer PF Contribution | 3,000 | 25,000 × 12% |

| Employer EPS Contribution | 2,083 | 25,000 × 8.33% |

Example 2: ₹15,000 Wage Ceiling Case

For an employee earning ₹15,000, the contribution is capped at ₹15,000.

| Salary Component | Amount (₹) | Calculation |

|---|---|---|

| Basic Salary + DA | 15,000 | |

| Employee PF Contribution (12%) | 1,800 | 15,000 × 12% |

| Employer PF Contribution | 1,800 | 15,000 × 12% |

| Employer EPS Contribution | 1,250 | Capped at ₹1,250 |

How to Calculate PF on Salary Above ₹15,000?

Wage Ceiling Rule Explained

For employees earning above ₹15,000, the contributions are capped at ₹15,000 for PF and EPS calculations. However, employers can opt for a higher voluntary contribution for the employee’s PF.

Higher PF Contribution Option

Employees earning above ₹15,000 can opt for a Voluntary Provident Fund (VPF) to increase their PF contribution.

Impact on Take-Home Salary

Voluntary contributions to the PF can affect an employee’s take-home salary. However, the increased savings will benefit the employee in the long term.

How is EPF Interest Calculated?

EPFO declares interest annually.

Interest is calculated on:

-

Monthly running balance

-

Credited at end of financial year

PF uses compound interest, meaning:

Interest earns interest.

This is why starting early is powerful.

How to Calculate PF Balance Online?

You can calculate your PF balance easily using the EPF online calculator tools available on the EPFO website. These tools require your basic salary, DA, and years of service to give an accurate estimate.

Tax Benefits of PF Contributions

| Tax Benefits | For Employees | For Employers |

|---|---|---|

| Section 80C Deduction | Contributions to EPF are eligible for a deduction under Section 80C of the Income Tax Act. | Employers also enjoy tax benefits on their contributions to EPF. |

| Tax-Free Interest | The interest earned on EPF is tax-free. | |

| Tax-Free Maturity Amount | The maturity amount is exempt from tax, subject to certain conditions. |

Common Mistakes in PF Calculation

-

Calculating PF on CTC instead of basic + DA

-

Incorrect employer split in contributions

-

Ignoring the wage ceiling rule

-

Failing to update salary changes

Why Understanding PF Calculation Formula is Important

Understanding the PF calculation formula helps in:

-

Financial Planning: Ensuring adequate retirement savings.

-

Retirement Corpus Estimation: Estimating how much you’ll have saved at retirement.

-

Salary Negotiation Clarity: Negotiating a salary package with a clear understanding of PF contributions.

-

HR Compliance: Helping HR ensure legal compliance with EPF rules.

Frequently Asked Questions (FAQs)

Is PF mandatory for all employees?

Yes, if working in an eligible organization under EPF Act.

Can an employee increase their PF contribution?

Yes, through Voluntary Provident Fund (VPF).

What happens if salary exceeds ₹15,000?

EPS contribution remains capped at ₹15,000 unless opted otherwise.

What is EPF eligibility?

Employees earning up to ₹15,000 must enroll, while others may choose to opt in voluntarily.

Conclusion

Understanding the PF calculation formula is crucial for both employees and employers to ensure accurate contributions and compliance with EPF regulations.

When you understand how to calculate PF clearly, you can apply it effectively.

-

You can verify whether your employer is deducting the correct amount

-

You can estimate your long-term retirement corpus

-

You can plan your tax savings more efficiently

-

You avoid salary structure confusion

For working professionals who want to understand salary components, deductions, and real in-hand salary breakdowns, you can explore more detailed guides on Career Salary Hub at 👉 https://careersalaryhub.com/

The platform covers practical salary insights, payroll explanations, and financial planning resources designed specifically for Indian employees.

By calculating PF correctly, employees gradually build a reliable retirement fund, while employers fulfill their statutory responsibilities under EPF rules.

Remember — PF is not just a deduction. It’s a disciplined wealth-building tool backed by the government.

Post Comment